How to screen investment opportunities at scale

Learn how to evaluate investment opportunities with a scalable framework. Our guide for VC analysts covers thesis design, automated screening, and analysis.

To screen investment opportunities well, you need a disciplined, scalable process. It all starts with a crystal-clear investment thesis. Think of this as your filter—it helps you instantly screen deals based on your specific criteria like founder profile, geography, or market type. This way, you're only spending precious time on companies that actually fit your fund's strategy.

Taming the Flood of VC Deal Flow

The venture capital world is completely saturated. For a VC analyst, the reality is a never-ending stream of pitch decks and cold emails. With more founders than ever and AI making it easy to start companies, what used to be a manageable flow has turned into an overwhelming flood of noise. It's a core challenge for VCs: how do you screen hundreds or thousands of opportunities per month or quarter?

Screening this volume is now the norm at many firms. This sheer volume is the core challenge in modern VC: how do you find the real signal in a sea of noise? The goal isn't just to stay afloat; it's to build a system that consistently finds high-conviction investments.

The Pitfalls of Manual Screening

Trying to sift through this volume manually isn't just inefficient; it’s a recipe for burnout and missed deals. When an analyst is buried, important details get missed and decision fatigue kicks in. This pressure cooker environment creates some serious problems that can drag down a fund's performance.

The main challenges of high-volume deal flow boil down to this:

-

Analyst Burnout: The repetitive, high-stakes grind of reviewing every single pitch deck leads to exhaustion. When that happens, the quality of your analysis tanks.

-

Thesis Drift: When you're overwhelmed, it’s tempting to chase exciting but off-strategy opportunities. Before you know it, you've strayed from your fund's core focus.

-

Inconsistent Evaluation: Without a structured process, deals get judged subjectively. This opens the door to biases and means your firm's investment criteria aren't applied consistently.

A disciplined, scalable screening process is no longer a luxury—it’s a necessity for survival and success. The best venture firms don't just find good deals; they build a machine that finds good deals over and over again.

This is where a methodical approach is non-negotiable. Instead of just reacting to every email that comes in, top-performing analysts design a repeatable process to screen opportunities at scale. Tools like Row Sherpa can help automate the grunt work, making this process smooth and automated.

This mindset shift—from manually evaluating one-by-one to systematically screening—is the first real step toward building a sustainable edge. It helps you move faster, make smarter decisions, and focus your valuable time on the deals that actually matter.

Building Your Investment Thesis as a Filter

You can't find what you're looking for if you don't know what it is. A good screening process starts with a razor-sharp, actionable investment thesis. This isn't some vague mission statement for your website; it's a codified set of rules that acts as your first, most powerful filter.

With the explosion of new founders and AI-driven startups, the volume of inbound deals can feel endless. A well-defined thesis is your defense against this noise. It lets you move from subjective "gut feelings" to a disciplined framework, instantly flagging misaligned deals and surfacing the ones that truly fit. This clarity is the foundation for any repeatable screening workflow.

Codifying Your Ideal Investment Profile

The first step is moving from abstract ideas to concrete criteria. Your thesis needs to be specific enough that any analyst on your team could apply it consistently. This means breaking down exactly what an ideal investment looks like for your fund.

Key components of an actionable thesis usually include:

-

Founder Archetype: Are you looking for repeat entrepreneurs with a previous exit? Or technical founders with deep domain expertise? Maybe it's first-time founders with a unique insight into a niche market.

-

Geography: Do you invest only in specific hubs like Silicon Valley or New York? Or are you focused on emerging tech ecosystems in the Southeast or Midwest? Be precise.

-

Sector and Industry: Define your target sectors with clarity. Instead of just "B2B SaaS," get specific: "B2B SaaS for regulated industries like finance and healthcare."

-

Business Model: Do you focus on high-margin software, deep tech with significant IP, or marketplace models? Each has totally different metrics and milestones that matter.

-

Traction Benchmarks: What are your minimums to even consider a company? This could be a specific ARR (like $100k - $500k ARR), a certain number of active users, or clear evidence of product-market fit through engagement metrics.

Defining these elements creates a clear profile of the companies you want to see. It transforms your thesis from a guiding philosophy into a practical screening tool.

Identifying Your True Predictors of Success

Not all criteria are created equal. The next level of building a strong thesis is understanding which criteria are the best predictors of success for your fund's specific strategy. This requires looking back at your best—and worst—investments to find the patterns.

A great investment thesis is a living document. It's built on a core set of beliefs but refined over time with data from both your successful investments and, just as importantly, the ones you missed.

For example, a deep tech fund might find that the most critical predictor isn't early revenue but the defensibility of the team's IP and the pedigree of its technical talent. In contrast, a consumer-focused fund might prioritize early signs of viral growth and user love, even if monetization is still a question mark.

Think about which signals consistently lead to the deals you actually want to evaluate. Is it a specific founder background? A particular go-to-market motion? A unique insight into an unbundling market? Pinpointing these predictors allows you to weigh criteria appropriately during your initial screen.

To make this tangible, here's how you might structure these predictors within your thesis.

Investment Thesis Criteria Breakdown

This table shows a sample framework for turning abstract thesis pillars into concrete, scorable criteria that directly link to what you believe drives success.

| Thesis Pillar | Specific Criteria Example | Why It's a Key Predictor |

|---|---|---|

| Founder-Market Fit | Founder has 5+ years of direct experience working inside the target industry. | Signals deep, non-obvious insights into the customer's pain point, not just a surface-level understanding. |

| Capital Efficiency | The company achieved $1M ARR with less than $500k in total funding raised. | Demonstrates strong product-market fit and an ability to grow without relying heavily on paid acquisition. |

| Market Timing | The market is undergoing a clear technological or regulatory shift (e.g., new privacy laws, AI adoption). | Indicates an external tailwind that can accelerate growth, making the go-to-market motion easier and cheaper. |

| Product Defensibility | The product benefits from strong network effects or has proprietary data assets. | Creates a durable competitive advantage that is difficult for competitors to replicate with capital alone. |

By defining your thesis this way, you create a system for evaluation rather than a collection of loose guidelines.

Once you have this clarity, you can set up a repeatable process. You can then use tools like Row Sherpa to automate the initial screening, applying your thesis at scale to categorize and score hundreds of deals, ensuring only the most relevant opportunities make it to your desk.

Designing a Disciplined and Repeatable Screening Process

You've got a well-defined investment thesis. That's your compass. Now you need to build the machinery to follow that compass consistently across hundreds, if not thousands, of inbound deals.

The goal is to move from a reactive, ad-hoc review process to a structured, multi-stage workflow. A system that methodically surfaces the best opportunities while efficiently filtering out the noise. This is where many investors, even sharp ones, falter. They have a brilliant thesis on paper but lack the operational discipline to execute it at scale.

A repeatable screening process ensures every company gets the same level of initial scrutiny, which helps remove human bias and decision fatigue. It’s about building a system that works for you, not the other way around.

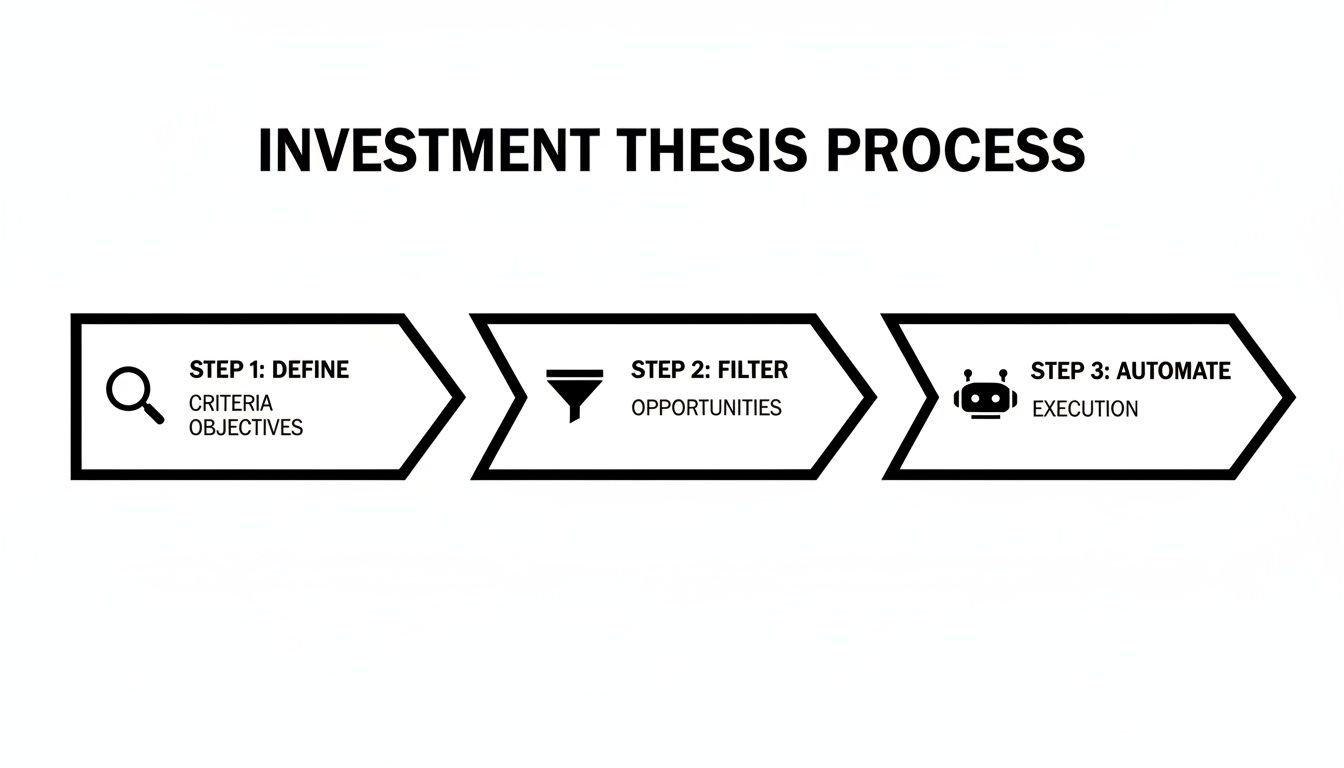

The flow is simple but powerful: define your criteria, filter opportunities based on those rules, and automate the execution wherever possible.

This diagram highlights a critical truth: a great screening system is a funnel, not a checklist. It's designed to disqualify deals that don't fit, freeing up your mental bandwidth to go deep on the ones that actually have a shot.

Structuring a Multi-Stage Triage System

The first step in building this machinery is creating a triage system. Not every deal deserves a deep dive right out of the gate. An effective process filters opportunities through progressively more intensive stages of review.

A common workflow might look something like this:

-

Initial Intake & Tagging: This is the top of your funnel where every deal lands. The goal here is simple: sort and tag. Is it B2B SaaS? FinTech? Within your target geography? Most of this initial sorting can and should be automated.

-

First-Pass Thesis Alignment: Next, you apply your core, non-negotiable criteria. If a company is outside your defined sector, stage, or traction benchmarks, it's a quick "no." This filter alone should eliminate 60-70% of inbound deal flow with minimal effort.

-

Detailed Analysis & Scoring: Companies that make it through the first pass move to a more detailed review. Here, you'll score them against the nuanced predictors in your thesis—things like founder-market fit, capital efficiency, market timing, and defensibility.

-

Partner Review: Only the highest-scoring companies should make it to a partner's desk. This simple step ensures that your senior team members are only spending their valuable time on pre-vetted, high-potential opportunities.

This multi-stage approach is all about protecting your most valuable resource—time—and allocating it to the deals with the highest probability of success.

Applying Automation to Your Screening Workflow

Trying to run this triage process manually across thousands of companies is an operational nightmare. It's slow, prone to error, and a surefire path to analyst burnout. This is where automation tools become a critical part of the modern investor's toolkit.

Platforms like Row Sherpa are designed to handle the heavy lifting of those initial screening stages. Instead of an analyst manually reading every single pitch deck to categorize a company or check its revenue, you can use AI-driven batch processing to do the work for you.

You can take a simple CSV of inbound deals, apply a consistent set of instructions to every row, and turn that unstructured data into a neatly categorized and scored list.

By uploading a list of companies, you can instruct the system to automatically categorize each one by industry, check if its stated ARR meets your threshold, and even provide an initial score based on how well it aligns with your investment thesis. A task that once took a week of manual data entry can now run in the background.

The real power of automation in deal screening isn't just speed; it's consistency. An AI model applies your thesis criteria with perfect discipline every single time, eliminating the human bias that can creep in on a Friday afternoon after reviewing 100 pitch decks.

This approach lets you build a truly scalable screening engine. Your role shifts from being a data processor to a strategic analyst. You get to spend less time on mundane tasks and more time on what really matters: building relationships with founders, understanding market dynamics, and conducting the deep, qualitative due diligence that machines simply can't replicate.

Example: turning raw deal flow into a ranked shortlist

In practice, this process often starts with a simple CSV exported from a CRM or inbound form: company name, website, sector, stage, and a short founder blurb. This can also be a list of founder profiles extracted from Linkedin through various scrapping tools such as Phantombuster.

Instead of evaluating each opportunity manually, analysts can enrich this dataset in batch - adding standardized fields such as company category, estimated headcount, funding history, business model, and target customer. Once enriched, the same dataset can be scored with LLMs against the fund’s thesis (e.g. “B2B infra, post-PMF, enterprise buyer”) to quickly surface the 10–20% of opportunities that warrant deeper work. This approach turns early-stage evaluation from a series of one-off judgments into a repeatable filtering mechanism, where analyst time is spent interpreting signals rather than assembling them.

Creating a Feedback Loop to Sharpen Your Thesis

A great screening process isn't static—it learns and adapts. Think of your investment thesis as a powerful filter. If you never clean or upgrade that filter, it will inevitably develop blind spots. In venture capital, where markets pivot overnight and new technologies appear out of nowhere, a static thesis is a serious liability.

The best VCs I know treat their screening process less like a set of rigid rules and more like a living system that gets smarter with every deal they see. This isn't accidental; it requires building a rigorous, disciplined feedback loop. The goal is simple but powerful: systematically analyze your decisions, spot patterns in your misses, and constantly sharpen your ability to predict what's next.

This isn't just about tweaking a few criteria on a scorecard. It's about building an institutional memory that compounds your fund’s intelligence over time. Without this loop, you're just running the same playbook over and over, hoping for a different outcome.

Moving Beyond Simple Conversion Rates

Plenty of firms track basic funnel metrics, like the percentage of deals that move from an initial screen to a full partner meeting. That's fine for gauging operational efficiency, but it tells you almost nothing about the quality of your decisions.

A high conversion rate might just mean your initial filter is too loose, wasting senior partners' time on deals that were never going to be a fit.

To get to the real insights, you have to track metrics that measure predictive accuracy. This means looking outward at the market, not just inward at your own pipeline.

Some KPIs that actually matter for a feedback loop:

-

Pass Rate by Thesis Pillar: Which of your core beliefs (e.g., founder with specific background, certain market size, a particular business model) is causing the most "no" decisions? This can quickly reveal if one of your filters is way too restrictive or outdated.

-

Time-to-Decision: How long are deals you ultimately pass on sitting in your pipeline? A long "time-to-no" is toxic and can seriously damage your firm's reputation with founders.

-

Source Performance: Which sources—inbound, your scout network, specific angel investors—are generating deals that consistently clear your initial screen? This tells you exactly where to double down on your sourcing efforts.

These metrics give you a health check on your process, but the most potent lessons come from studying the deals you let get away.

Evaluate Your Coverage

Efficient measurement of your coverage is essential to gauge your progress and effectiveness. Recognizing the opportunities that your current sourcing efforts may have overlooked is key to ensuring the quality of deal flow and, subsequently, performance. The strength of venture capital firms depends largely on the quality of opportunities they explore.

To achieve this, consider utilizing data sources like Crunchbase, Pitchbook, or Dealroom, or keeping an eye on tech media that report fundraising deals. It’s crucial to filter deals that align with your investment thesis. Don't hesitate to rely on platforms such as Row Sherpa to handle the complex task of classifying companies on a large scale and identifying those that fit your criteria.

Conducting Rigorous Anti-Portfolio Analysis

The most crucial—and most humbling—part of any feedback loop is the anti-portfolio analysis. This is the disciplined practice of tracking and studying the companies you passed on that later went on to raise significant funding from other top-tier firms.

A formal anti-portfolio review is the single best way to confront your fund's biases and blind spots. It forces you to ask the hard questions like, "how many deals got funded that we didn't see? and why?".

A systematic review process prevents this from becoming an informal, anecdotal gripe session. You need a structured approach to find the root cause of your "misses." Was the decision a flaw in your thesis, a misreading of the market, or just a simple breakdown in your operational process?

Here’s a practical framework for getting it done:

-

Track Every "No": For every company you pass on, log it. More importantly, write down a concise reason for the pass that ties directly back to your investment thesis. No generic reasons.

-

Set Up Alerts: Use market intelligence tools like Crunchbase or PitchBook to get notified the moment a company you passed on announces a new funding round.

-

Perform a Root-Cause Analysis: When a "miss" gets flagged, it's time for a post-mortem. Dig in and figure out what happened. Was it a...

-

Thesis Failure? The company succeeded despite not fitting your core criteria. Maybe your definition of a "great founder" is too narrow, or you're underweighting a new go-to-market strategy that's starting to work.

-

Market Misread? You underestimated the TAM or the growth rate of the market. This happens all the time with companies creating entirely new categories.

-

Operational Failure? The deal simply slipped through the cracks. Maybe your response time was too slow, or the right partner never even saw it.

-

This disciplined review turns every missed opportunity from a source of regret into a valuable lesson. It provides the raw data you need to refine your thesis, making it more resilient and accurate for the next wave of deals. By learning from the deals you didn't do, you dramatically improve your ability to spot the ones you absolutely should.

VC Deal Screening: Your Questions Answered

Even with a killer process, you'll always have questions. Building a deal screening system that actually works means refining it over time. Here are some of the most common challenges I've seen analysts face, along with some straight answers.

How Can I Screen Deals Faster Without Sacrificing Quality?

Stop thinking about "moving faster" and start thinking about "focusing your time better."

The secret isn't some magic trick; it's a combination of a brutally strict investment thesis and some smart automation. First, define your non-negotiables. These are the absolute deal-breakers for sector, stage, geography, and founder profile. This becomes your most ruthless initial filter. If a deal doesn't tick these boxes, it's out. No exceptions.

Then, you bring in tools to automate the initial data enrichment and scoring based on that thesis. This simple move completely shifts your role from manual data entry to strategic oversight. You'll spend your valuable time doing a deep, qualitative review of only the most promising opportunities—the ones that already cleared your automated hurdles.

What Are the Most Common Mistakes in Deal Screening?

You can trip up in a lot of places, but a few mistakes are particularly common and can absolutely torpedo a fund's performance.

-

Thesis Drift: This is the big one. It happens all the time. An analyst gets swept up in a compelling story or a super impressive founder, even when the company is a terrible fit for the fund's strategy. This wastes everyone's time and dilutes the fund’s focus.

-

Relying on Gut Feel: Look, intuition has its place. But leaning on it too heavily without a data-driven process is just asking for bias to creep in. A structured, repeatable screening process ensures every deal gets judged on the same core merits, period.

-

No Feedback Loop: The single biggest long-term error is failing to track your anti-portfolio—the great deals you passed on. If you're not analyzing your misses, you can't learn from them. Your screening accuracy will simply never get better.

One of the greatest mistakes is allowing a charismatic founder to pull you away from your thesis. Discipline in the screening process is what separates good analysts from great ones; it ensures that excitement is validated by strategy, not driven by emotion.

How Much Weight Should I Give the Founding Team Versus the Market?

Ah, the classic VC debate. The truth is, most experienced investors will tell you they're both critical filters. You can't have one without the other.

An exceptional team can pivot, navigate a tough market, and find a way to win. They have the resilience and ingenuity to overcome obstacles that would sink a lesser crew.

But on the other hand, a massive, growing market with a powerful tailwind can practically pull an average team to success. The market's momentum just creates so many opportunities.

Your initial screen has to filter for both. You need a market that fits your thesis and has real potential for explosive growth. At the same time, you're looking for a founding team that shows clear signs of resilience, deep domain expertise, and a proven ability to actually get things done.

A great team in a dead market is a bad investment. So is a weak team in a great market.

Ready to stop drowning in spreadsheets and start screening deals at scale? Row Sherpa helps you automate the entire process. Upload your deal flow, apply your investment thesis with a simple prompt, and get back enriched, scored, and categorized data in minutes. Learn more and try it for free at RowSherpa.com.